All Categories

Featured

Table of Contents

Mobile homes are thought about to be individual residential or commercial property for the purposes of this section unless the proprietor has de-titled the mobile home according to Area 56-19-510. (d) The building must be marketed available at public auction. The promotion should remain in a paper of general blood circulation within the area or district, if appropriate, and must be qualified "Delinquent Tax Sale".

The advertising needs to be published when a week prior to the lawful sales day for three consecutive weeks for the sale of real estate, and two successive weeks for the sale of personal effects. All costs of the levy, seizure, and sale needs to be included and collected as added prices, and should consist of, however not be limited to, the expenses of seizing genuine or personal effects, advertising and marketing, storage space, determining the limits of the home, and mailing licensed notices.

In those situations, the police officer may dividing the property and furnish a legal description of it. (e) As a choice, upon authorization by the county regulating body, an area might use the procedures given in Chapter 56, Title 12 and Section 12-4-580 as the initial step in the collection of delinquent taxes on real and personal effects.

Result of Change 2015 Act No. 87, Section 55, in (c), substituted "has de-titled the mobile home according to Section 56-19-510" for "offers written notification to the auditor of the mobile home's addition to the land on which it is situated"; and in (e), put "and Area 12-4-580" - overage training. SECTION 12-51-50

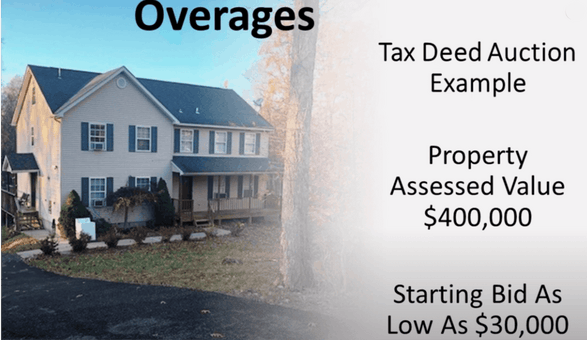

What Is The Best Course For Learning Property Overages?

The surrendered land compensation is not called for to bid on residential or commercial property known or sensibly thought to be polluted. If the contamination ends up being understood after the quote or while the payment holds the title, the title is voidable at the political election of the payment. HISTORY: 1995 Act No. 90, Section 3; 1996 Act No.

Settlement by successful bidder; receipt; disposition of profits. The effective bidder at the delinquent tax sale will pay lawful tender as given in Section 12-51-50 to the person officially charged with the collection of overdue taxes in the sum total of the bid on the day of the sale. Upon repayment, the person formally billed with the collection of overdue taxes shall equip the purchaser an invoice for the purchase money.

Expenses of the sale have to be paid initially and the balance of all overdue tax sale monies collected have to be committed the treasurer. Upon receipt of the funds, the treasurer will note right away the general public tax obligation documents concerning the residential property offered as follows: Paid by tax obligation sale hung on (insert day).

How Do I Find The Best Real Estate Training Resources?

166, Area 7; 2012 Act No. 186, Area 4, eff June 7, 2012. SECTION 12-51-80. Settlement by treasurer. The treasurer shall make complete settlement of tax sale monies, within forty-five days after the sale, to the particular political class for which the taxes were levied. Profits of the sales in excess thereof must be kept by the treasurer as or else provided by law.

166, Area 8; 2015 Act No. 87 (S. 379), Area 57, eff June 11, 2015. (A) The skipping taxpayer, any kind of grantee from the proprietor, or any kind of home mortgage or judgment lender may within twelve months from the day of the overdue tax sale redeem each product of genuine estate by paying to the person formally billed with the collection of overdue taxes, analyses, charges, and prices, with each other with interest as given in subsection (B) of this section.

What Is The Most Comprehensive Course For Understanding Tax Lien?

334, Section 2, gives that the act relates to redemptions of building sold for overdue tax obligations at sales hung on or after the effective date of the act [June 6, 2000] 2020 Act No. 174, Areas 3. A., 3. B., supply as follows: "SECTION 3. A. real estate workshop. Regardless of any other provision of law, if actual building was sold at a delinquent tax sale in 2019 and the twelve-month redemption period has actually not run out as of the efficient day of this area, then the redemption duration for the real estate is extended for twelve additional months.

For objectives of this phase, "mobile or manufactured home" is specified in Area 12-43-230( b) or Area 40-29-20( 9 ), as relevant. HISTORY: 1988 Act No. 647, Section 1; 1994 Act No. 506, Area 13. SECTION 12-51-96. Problems of redemption. In order for the proprietor of or lienholder on the "mobile home" or "made home" to redeem his residential property as allowed in Section 12-51-95, the mobile or manufactured home based on redemption should not be gotten rid of from its location at the time of the delinquent tax obligation sale for a duration of twelve months from the day of the sale unless the proprietor is required to relocate by the individual apart from himself that possesses the land upon which the mobile or manufactured home is situated.

If the owner moves the mobile or manufactured home in offense of this section, he is guilty of a violation and, upon sentence, should be penalized by a penalty not exceeding one thousand bucks or imprisonment not exceeding one year, or both (training) (investing strategies). In addition to the other demands and repayments needed for an owner of a mobile or manufactured home to retrieve his property after a delinquent tax sale, the skipping taxpayer or lienholder likewise have to pay rent to the purchaser at the time of redemption a quantity not to surpass one-twelfth of the tax obligations for the last completed residential property tax year, special of penalties, prices, and interest, for every month between the sale and redemption

For objectives of this rental fee estimation, greater than one-half of the days in any month counts as an entire month. HISTORY: 1988 Act No. 647, Area 3; 1994 Act No. 506, Area 14. AREA 12-51-100. Cancellation of sale upon redemption; notice to buyer; reimbursement of acquisition cost. Upon the property being redeemed, the person officially billed with the collection of overdue taxes shall terminate the sale in the tax obligation sale book and note thereon the amount paid, by whom and when.

Tax Lien

Personal residential property shall not be subject to redemption; buyer's expense of sale and right of belongings. For individual residential or commercial property, there is no redemption period succeeding to the time that the residential or commercial property is struck off to the effective buyer at the delinquent tax obligation sale.

Recovering surplus funds from tax sales has become a lucrative industry, made possible by accessible training like "tax overages. This comprehensive training covers everything, including how to create an overages database to navigating the legal processes required for recovery. With his guidance, students can target profitable regions for overages recovery and develop a sustainable business model. Whether you’re just starting out or seeking to grow your business, Bob Diamond’s expertise will guide you to success.HISTORY: 1962 Code Area 65-2815.10; 1971 (57) 499; 1985 Act No. 166, Section 11. AREA 12-51-120. Notification of approaching end of redemption period. Neither more than forty-five days neither less than twenty days before completion of the redemption period genuine estate marketed for tax obligations, the person officially billed with the collection of overdue tax obligations shall send by mail a notice by "qualified mail, return receipt requested-restricted distribution" as provided in Area 12-51-40( b) to the skipping taxpayer and to a grantee, mortgagee, or lessee of the home of record in the suitable public records of the county.

{kind=link}

Table of Contents

Latest Posts

Delinquent Tax Sale

Tax Lien Investing Expert

Tax Lien Certificates List

More

Latest Posts

Delinquent Tax Sale

Tax Lien Investing Expert

Tax Lien Certificates List